Ich werde die nächsten Tagen in UK verweilen. Denke das ich Anfang März wieder online sein werde.

Porsche draws on €10bn pre-crunch loan FT

Porsche draws on €10bn pre-crunch loan FT

Porsche also made large amounts of money from currency hedging earlier this decade and some analysts have suggested that it is behaving more like a hedge fund than a carmaker.

Although Porsche denied its action had any bearing on its plans for Volkswagen – which have been thrown into confusion by the German government proposing a law protecting Europe’s largest carmaker – it will give it a war-chest on top of its considerable cash reserves to buy further shares when it pleases.

Porsche führt Hausbanken vor

Der Autobauer Porsche düpiert die Banken in deren Kerngeschäft. Das Stuttgarter Unternehmen teilte mit, eine Kreditlinie von 10 Mrd. Euro voll auszuschöpfen, um das Geld nun "risikofrei" und "gut verzinslich" anzulegen. Damit hatten die Geldhäuser nicht gerechnet.

Eigentlich hatten die Banken den Schwaben den Kreditrahmen gewährt, um einen möglichen Kauf von VW-Aktien abzusichern. Mit dem Deal tummelt sich der Sportwagenhersteller erneut jenseits seines Hauptgeschäfts, um stattdessen auf dem Finanzmarkt Geld zu verdienen. Bereits im vergangenen Jahr hatte Porsche mit Optionsgeschäften auf VW-Aktien 3,6 Mrd. Euro Gewinn gemacht. Finanzchef Holger Härter hatte bei den damaligen Wetten auf den VW-Kurs die Spezialisten der Finanzbranche geschlagen.

Wenn Porsche die günstig geliehenen 10 Mrd. Euro nun zu besseren Konditionen anlegt, bereichert sich der Konzern schon wieder auf Kosten der Banken - darunter die Frankfurter Commerzbank. Die Experten der Landesbank Baden-Württemberg (LBBW) schätzen, dass Porsche mit einem Zinsvorteil von 0,2 bis 0,3 Prozentpunkten rechnen kann - was in einem Jahr einen Gewinn von 20 bis 30 Mio. Euro ergeben würde. "Geld leihen und anlegen ist eigentlich Bankgeschäft und gehört nicht originär zu einem Autohersteller. Aber Porsche hätte Geld verschenkt, wenn sie das nicht gemacht hätten", sagte LBBW-Analyst Frank Biller.

Allerdings könnte der Deal das Klima zwischen den Stuttgartern und ihren Hausbanken belasten. "Das kann sich nur ein sehr solides Unternehmen mit guten Beziehungen zu seinen Banken leisten", sagte Willem Sels, Leiter der Kreditanalyse von Dresdner Kleinwort.

Die von Porsche jetzt gezogene Kreditlinie war im Frühjahr 2007 ausgehandelt worden - vor dem Ausbruch der internationalen Finanzkrise. Damals waren die Konditionen deutlich günstiger. Offenbar nutzen derzeit neben Porsche auch andere Unternehmen die Möglichkeit, einstmals günstig ausgehandelte Kreditgarantien zum Nachteil der Banken zu verwenden. "Von Investoren war zu hören, dass es Firmen gibt, die das Gleiche tun", sagte Sels.

Leidtragende sind die Banken: Sie müssen den Unternehmen Kredite zu Billigkonditionen gewähren, am Kapitalmarkt aber sehr viel höhere Zinsen bieten, um an Geld zu kommen. Angesichts des scharfen Wettbewerbs um gute Firmenkunden können sich die Institute kaum dagegen wehren - juristisch ohnehin nicht, aber auch nicht durch Nachverhandlungen.

Der Kreditrahmen von Porsche lag ursprünglich bei 35 Mrd. Euro. ABN Amro, Barclays Capital, Merrill Lynch, UBS und die Commerzbank hatten die Kreditlinie arrangiert. Mit dem Geld sicherte Porsche sein Pflichtangebot für VW-Aktien ab, nachdem die Stuttgarter ihren Anteil an VW Ende März 2007 auf 31 Prozent erhöht hatten. Durch das Überschreiten der 30-Prozent-Schwelle war die Pflichtofferte zwingend. Mit einer rechtlich zwar korrekten, de facto aber viel zu niedrigen Offerte hatte Porsche das Pflichtangebot absichtlich scheitern lassen, um nicht viele Milliarden auf einen Schlag ausgeben zu müssen.

Weil der Autobauer die 35 Mrd. Euro schwere Kreditlinie damit nicht mehr benötigte, senkte man die Garantien auf 10 Mrd. Euro herab. Dabei handelte Porsche mit den Banken eine Umwidmung auf "allgemeine geschäftliche Belange" aus; dadurch war das Darlehen nicht mehr an den Kauf von VW-Aktien gebunden.

Porsche hält derzeit 31 Prozent an VW, hat sich aber mit Optionen den Kauf weiterer Anteile gesichert. Bisher gibt es noch keinen Aufsichtsratsbeschluss, über die 50-Prozent-Schwelle zu gehen. LBBW-Analyst Biller glaubt nicht, dass die nun angelegten 10 Mrd. Euro für den Kauf von VW-Anteilen genutzt werden: "Porsche wird den jährlichen und risikofreien Gewinn mitnehmen und sich gegebenenfalls einen neuen Kredit holen."

FT Alphaville So either they couldn’t make it work, or in the end they didn’t want to. Nine days ago, Standard Chartered withdrew the liquidity support promised (conditionally) to its $7bn Whistlejacket SIV, after the vehicle breached its net asset value trigger, and appointed a receiver, Deloitte.

FT Alphaville So either they couldn’t make it work, or in the end they didn’t want to. Nine days ago, Standard Chartered withdrew the liquidity support promised (conditionally) to its $7bn Whistlejacket SIV, after the vehicle breached its net asset value trigger, and appointed a receiver, Deloitte.This is as a result of a number of factors, including the pace of continuing deterioration in the market for certain asset classes and the impracticality of completing any proposal within the confines of the receivership as it has evolved.Oh dear. This looks doubly bad. Whistlejacket tripped its trigger because the value of its assets fell below 95 per cent of par - or 50 per cent of the face value of the notes after leverage - triggering automatic receivership and liquidation.

While Deloitte say that a firesale is not an option (”absolutely categorically no need“), and that is still seeking other solutions, time is getting tight. The receiver elected last Friday not to pay the medium term notes maturing that day. S&P lowered its rating on the notes to CCC-, and its issuer rating on Whistlejacket, as a result - and said that as the notes have a three-day grace period payment default will take place on Thursday 21. Or tomorrow.

> It looks like the statement via Ft Alphaville SIVs don’t rollover, they die isn´t far off the mark....... And the chart might give an impression what still needs to be refinanced......

> Es sieht so aus als wenn die Aussage von Ft AlphavilleSIVs don’t rollover, they die das ganze recht treffend zusammenfaßt.....Der nachfolgende Chart gibt einen ganz nettenn Überblick über die kommende Refinanzierungswelle die mehr denn je in den Sternen steht......

As one who has listened to the entire conference call from Credit Suisse just one week ago i can assure you that this will spook the markets. Credit Suisse was besides Deutsche Bank and Goldman Sachs viewed as one of the big winners during the turbulence. But there was always doubt that their numbers might be too good to be true...... Credit Suisse is proving that this might be the case..... Should be very bad news for the confidence in the marketplace overall...... I assume the "arrogance" from the Credit Suisse management won´t be as obvious as during the last call...... Stock tanking 7 percent......

Als einer der sich vor einigen Tagen die Telefonkonferenz angehört at bin ich mir sicher das diese Meldung hohe Wellen schlagen wird. Bisher galt die Credit Suisse zusammen mit der Deutsche Bank und Goldman Sachs als einer der Gewinner der Marktturbulenzen. In der Vergangenheit sind immer wieder Zweifel aufgekommen ob "die Zahlen nicht zu gut sind um wahr zu sein" ...... Credit Suisse liefert hier eine Steilvorlage für diese Vermutung......Ich bin mir zudem sicher das die "Arroganz" von Seiten des Managements während der nächsten Telefonkonferenz sicher nicht wieder so ausgeprägt sein wird wie letzte Woche .... Aktie zur Eröffnung 7% tiefer......

Thanks to Randy Galsbergen

Thanks to Randy GalsbergenCredit Suisse Further to its commitment to provide transparency, Credit Suisse today announced that in connection with the operation of ongoing control processes, it has undertaken an internal review that has resulted in the repricing of certain asset-backed positions in its Structured Credit Trading business within Investment Banking.

The current total fair value reductions of these positions, which reflect significant adverse first quarter 2008 market developments, are estimated at approximately USD 2.85 billion (having an estimated net income impact of approximately USD 1.0 billion).

In the first quarter to date, we estimate we remain profitable after giving effect to these reductions. The final determination of these reductions will depend on further results of our review and continuing market developments. We will also assess whether any portion of these reductions could affect 2007 results. Finally, our internal review, which has identified mismarkings and pricing errors by a small number of traders in certain positions in our Structured Credit Trading business, is continuing.

> Here the Full Year Results from Feb. 12th & Webcast

Qatar was maybe a little bit premature....

Sieht ganz so aus als wenn einige Investoren heute leicht erhöhte Temperatur haben werden.....

Qatar fund buys Credit Suisse stake

The QIA’s move comes after Credit Suisse posted robust fourth-quarter results underscoring its resilience during the credit crisis,......

Thanks to Matt Davies

Thanks to Matt Davies

Economist Not all is lost for the structured-finance business. But it faces further discomfort before it can start to recover some of its past sheen

Economist Not all is lost for the structured-finance business. But it faces further discomfort before it can start to recover some of its past sheen Along the way, banks cooked up a simmering alphabet soup. The ingredients included collateralised-debt obligations (CDOs), which repackage asset-backed securities, and collateralised-loan obligations (CLOs), which do the same for corporate loans, as well as structured investment vehicles (SIVs) and conduits, which banks used to keep some of their exposure off their balance sheets.

Along the way, banks cooked up a simmering alphabet soup. The ingredients included collateralised-debt obligations (CDOs), which repackage asset-backed securities, and collateralised-loan obligations (CLOs), which do the same for corporate loans, as well as structured investment vehicles (SIVs) and conduits, which banks used to keep some of their exposure off their balance sheets.

The breakneck growth of this business went into reverse last summer, when it became clear that defaults would undermine the structures built around America's mortgage markets. So tarnished has the subprime-mortgage market become, because of shoddy loan underwriting and fraud, that investors are likely to shun securities linked to it for months if not years. Securitisation of better-quality “jumbo” mortgages—too big to be bought by government agencies—is also at a near-halt. “Mortgages were traditionally seen as very safe assets. Now all but the very best are stamped with a skull and crossbones,” says Guy Cecala, of Inside Mortgage Finance, a newsletter.

CDOs are unlikely to regain a following in a hurry (see chart 2). Still less popular are CDO-squareds (resliced and repackaged CDOs) and higher powers. CLOs have also been battered as the leveraged loans they are linked to have tumbled in value. However, their collateral is sounder than that backing subprime CDOs, being based on company financials rather than the blandishments of mortgage brokers.

The prospects for SIVs are bleaker still. SIVs borrow short-term to invest in long-dated assets; and investors will no longer tolerate such mismatches in vehicles shielded from standard banking regulation. With the disappearance of the SIVs' funding sources, notably asset-backed commercial paper, banks had to bring over $136 billion-worth onto their books. That comes on top of over $160 billion, so far, of subprime-related write-downs, over a third of which has come at three banks: Citigroup, Merrill Lynch and UBS.

Though few bankers worked in structured finance, it was a huge earner, accounting for 20-30% of big investment banks' profits before the crisis, according to CreditSights, a financial-research firm. Banks such as Bear Stearns, Lehman Brothers and Morgan Stanley, which bought or built mortgage-origination businesses to fuel the securitisation machine, have rushed to close or pare them. Merrill, whose fees from CDOs alone peaked at $700m in 2006, said recently that it would stop packaging mortgages altogether.

Alongside the banks, the “gatekeepers” who were supposed to lend stability and credibility to the new originate-and-distribute model of finance have also been found wanting. Rating agencies' models underplayed the risk that loans from different lenders and regions could turn sour at the same time. Bond insurers, too, misjudged the risks lurking in CDOs. That failing has undermined the worth of their guarantees and strained their own credit ratings—and hence financial markets.

George Miller, the ASF's executive director, accepts that this crisis of confidence will lead to a degree of “re-intermediation” for a time, as some banks go back to balance-sheet lending. But he insists that it highlights the dangers of lax lending standards in a particular market rather than fundamental faults in securitisation itself.

A study by NERA, an economic consultancy, commissioned by the ASF before the crunch, offers some support for this view. Preliminary results, based on data from 1990 to 2006, suggest that increased securitisation leads to lower spreads in consumer credit and softens interest-rate shocks for banks, especially smaller ones. On the other hand, in a recent paper two economists at the University of Chicago's business school conclude that securitisation encouraged mortgage originators to lend to dodgy borrowers.

Stresses and strains

What is not in doubt is that the subprime crisis has exposed four deep flaws in the practice of securitisation. The first is that by severing the link between those who scrutinise borrowers and those who take the hit when they default, securitisation has fostered a lack of accountability.

A debate has been rumbling over how to ensure that lenders have more “skin in the game”. Some think they should set aside a sliver of capital even for loans they sell on. Andrew Davidson, a structured-finance consultant, suggests an “origination certificate”, guaranteeing the quality of the underwriting, issued by the lender and broker, which stays with the loan. Alex Pollock of the American Enterprise Institute thinks that securitisers should be required to guarantee the quality of their loan pools, as are America's government-sponsored mortgage giants, Fannie Mae and Freddie Mac. Others counter that most such exposures can be neutralised these days through derivatives markets.

The second flaw is the sheer lack of understanding of some instruments. Not long ago investors took too much on trust. They are now clamouring for more “transparency”. Some want a central trade-quoting facility for lumpy asset-backed products: regulators have approached the New York Stock Exchange. CME Group, which runs the world's largest futures exchange, is also looking to expand its clearing of over-the-counter securities.

Yet reams of information already accompany mortgage-backed securities sold in public markets. Even SIVs provide a steadier stream of data to investors than most of the banks backing them. So some interpret calls for greater disclosure as whimpering by investors who did not do their homework.

However, more information about the performance of loans after origination would help, particularly those in leveraged structures such as CDOs. This opens up opportunities: fewer banks were at the ASF conference this year, but more data-analytics firms turned up. Clayton, the largest mortgage-surveillance company, unveiled a partnership with Experian, an information-services firm, that will help mortgage-servicers to package subprime loans for modification under a plan backed by the ASF and America's Treasury. Later, it hopes to offer a swathe of data to buyers of structured products.

Understanding the underlying assets is, or should be, at the core of securitisation. Securitisation is really an arbitrage: with surplus collateral, assets can be bundled into an entity with a supercharged credit rating. But if investors fail to spot the jiggery-pokery with credit scores and the outright fraud that permeated the subprime market, that cushion of safety quickly disappears. Witness the speed with which losses have spread into supposedly safe, “super senior” tranches of CDOs.

This points to the third flaw: that some securities were poorly structured, often because their risks were not fully understood. The upper layers of a well-designed securitisation vehicle should be all but impervious to loss. But poorly structured deals, like those stuffed with subprime and marginally less iffy “Alt-A” loans in 2006 and early 2007, have crumbled as the weakness of the collateral becomes clear.

The fourth flaw was the market's over-reliance on ratings as a short cut to assessing risk. In the go-go years, people wrongly assumed that an AAA-rated mortgage bond—even one with a high yield—would never lose value. But the rating agencies, paid for their appraisals by the seller not the buyer, were compromised from the start. Moreover, their quantitative models appear to have ignored “fat-tail” risks—the possibility that large losses are likelier than standard statistical models predict.

Though the agencies do not have to suffer giant write-downs, they have paid a high price. Before the market imploded, almost half the revenue of Moody's, a leading agency, came from structured finance. Now the agencies are revising their rating criteria in a bid to head off tougher regulation. “Either deals get less complex or we have to find a better shorthand for measuring risk,” says Ron Borod of Brown Rudnick, a law firm. The rating agencies say they were never supposed to substitute for investors' own due diligence. That is disingenuous, given their past self-assuredness. Still, wise investors will take future ratings with a pinch of salt, as most hedge funds have long done.

As the market grapples with change, some is likely to be imposed from above. Separately, international regulators and the President's Working Group (comprising America's Treasury, the Federal Reserve and others) are looking into securitisation's part in the crisis. By co-operating over loan modifications, the ASF may have gained favour with the working group.

The industry is more worried about two bills in America's Congress. Securitisers can live with much of the one that has been passed by the House of Representatives. What alarms them is an “assignee liability” provision that would hold them partly responsible for lax lending by originators. This, they say, would send a chill through secondary markets, cutting credit to thousands of worthy borrowers. Precedent is on their side. Georgia introduced assignee liability, only to back-pedal after the state's subprime market started to seize up. Not all bankers are against it: in Las Vegas, Bianca Russo of JPMorgan Chase argued that some form of it was needed to counter the perception, if not the reality, that securitisation was harmful.

The other bill would allow bankruptcy judges to alter the terms of struggling borrowers' mortgages. The industry argues that this would be an intolerable violation of the sanctity of loan-pooling contracts. In addition, securitisers face probes by several state attorneys-general, the Internal Revenue Service, the Federal Bureau of Investigation, the Securities and Exchange Commission and the Justice Department, as well as lawsuits from investors and a rising number of stricken municipalities.

Bankers will tell you that the subprime meltdown was just that: the product of irresponsible lending to, and borrowing by, flaky consumers, not a broader crisis of securitisation. Maybe, but the severity of the credit crunch points to broader pain ahead. More will come from housing: much of the 30-40% of American home-equity loans that have been securitised looks wobbly, as does a growing chunk of the $800 billion of Alt-A paper outstanding. Loans for offices are an even bigger worry. The spread on the AAA tranche of an index tracking bonds backed by commercial mortgages has tripled since the turn of the year. New issuance is frozen.

Trouble is also brewing for securities tied to non-mortgage consumer assets, such as credit-card debt, car loans and student loans, which make up a good slice of the asset-backed market (see chart 3). Credit-card delinquencies are creeping up as the economy turns down. The sharp slowdown in card borrowing, reported recently by the Fed, will mean less raw material for securitisation. Standards for car loans dropped in 2006-07, though not as dramatically as they did for mortgages.

One ominous sign is that structured instruments tied to student loans are coming unstuck, although the loans typically carry a federal guarantee. Recent auctions of such securities by Citigroup, Goldman Sachs and others have failed. Normally the banks would have bought in whatever did not sell. But they have declined, because they dare not cram even more assets onto their already strained balance sheets.

Yet securities of these types should be more resilient than those tied to subprime loans. Their structures are tried and tested, having evolved, along with performance data in their markets, over many years. In contrast, subprime mortgages with only a short record were shoved into many-layered structures that depended on house prices holding up. “They started from the other end entirely, asking how can we create CDOs, backed by mortgage-backed securities, themselves backed by collateral with barely any history, and their stress tests assumed house prices would be stable and the loans in the pools uncorrelated,” says Mr Borod.

Encouragingly, credit-card receivables are still being bundled and sold. There are even shoots of hope in the mortgage market, thanks to a refinancing mini-boom in the wake of interest-rate cuts—though most new deals are backed by the giant agencies, Fannie Mae and Freddie Mac, not Wall Street (see chart 4).> A reader points correctly out that this comment from the Economist could easily come from "the Socialist"

> Ein Leser weist mich zurecht darauf hin, das dieser Passus eher dem"Sozialisten" und nicht dem "Economist" gut zu gesicht stehen würde.

"Also, I don't see it as "encouraging" that debt risk is being concentrated in the GSEs, with their implied taxpayer guarantees. Especially now that they've upped the conforming limit. This is just another variation of socialized costs."

Thanks/Danke !

Saunter down the strip

It is also worth remembering that securitisation has not been confined to consumer and corporate loans. In the past decade financial engineers have found ways to package and sell tobacco-settlement and mutual-fund fees, sports and fast-food franchise rights, life-insurance premiums, intellectual property, music royalties and much more. Hollywood studios use securitisation to help finance film-making. With intangible assets accounting for an ever-growing share of corporate value, this trend looks likely to continue.

That may be scant consolation to the banks whose bets have gone so spectacularly wrong. Their fingers are still being singed by mortgage-backed securities and CDOs that continue to burn. Those hoping for a recovery face a long wait, maybe 18 months or more for out-of-favour collateral such as non-agency mortgages. Some once-enthusiastic cheerleaders are turning gloomy: Bear Stearns said recently that its net short position on subprime loans and bonds had risen to $1 billion. Others are redeploying staff and capital to fee businesses that don't put a strain on the balance sheet, such as merger advice.

But it would be a mistake to write the obituary of structured finance. Even its sternest critics accept that securitisation has brought real economic benefits, and that it would be wrong to throw away the whole barrel because of a few subprime apples. Some students of financial innovation think the market will come back even more inventive after scorching its less attractive pastures. “As with past forest fires in the markets, we're likely to see incredible flora and fauna springing up in its wake,” says Andrew Lo, director of the Massachusetts Institute of Technology's Laboratory for Financial Engineering.

So it may just be a matter of hanging on. As any punter in Las Vegas will tell you, every losing streak ends eventually, if you can only stay solvent for long enough.

Share buyback program Daimler

Share buyback program DaimlerIn order to optimize its capital structure, the Group initiated a share buyback program in August 2007. In this context, it was announced that up to €7.5 billion would be applied to buy back nearly 10% of the company’s own shares. By the middle of December 2007, 50 million shares had been acquired for €3.5 billion. These shares were canceled by the end of the year. The share buyback program will be continued today.

At least they hadn´t to issue new debt to finance this "smart" move.....

Immerhin muß Daimler im Gegensatz zu anderen diese Transaktion nicht mit neuen Schulden finanzieren....

The capital released through our securitisation activities over recent years has been used to expandour national and international lending business. Additionally, the capital has also been used to investing international loan portfolios. Two thirds of our investments are focused on US investment-gradeportfolios (including, for example, credit card claims,mortgage loan claims and corporate loans), with theremaining third being invested in similarly structured European portfolios.

Das durch die Verbriefung während der letzten Jahre freigesetzte Kapital haben wir für die Ausweitung unseres nationalen und internationalen Kreditgeschäftes genutzt. Darüber hinaus haben wir dieses Kapital verwendet, um in internationale Kreditportfolien zu investieren. Unsere Investments konzentrieren sich zu zwei Dritteln auf mindestens Investmentgrade-geratete US-Portfolios (wie zum Beispiel Kreditkartenforderungen, Hypothekenkreditforderungen sowie Unternehmenskredite) sowie zu einem Drittel auf europäische Portfolien mit ähnlichen Strukturen.

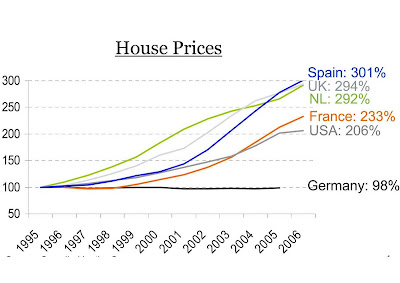

Global Property Guide The Irish property crash is worsening. Prices paid for second-hand apartments in Dublin fell by as much as 17% in 2007, and house prices in Dublin dropped by an average of 10% on the year, according to a review by the Irish Auctioneers and Valuers Institute (IAVI) (However Sherry Fitzgerald, an agent, reports a more moderate fall of 6.8% in 2007 on second-hand Dublin properties).

In the new apartment market, developers have been giving away cars, bathroom and kitchen suites in a vain effort to hold up prices. That is now starting to crack, as in January, two developers dropped prices 20% on two different developments. .....

Previously, house prices in Ireland had risen further and faster than those of any other country for which figures are reported, except Estonia, having risen for 17 years without a break.

Since 1996, when the surge began in earnest, national house prices rose from €75,000, to €287,664 (end-2006), i.e., a rise of 283% in nominal terms. House prices in Dublin rose even more during the same period, with a 366% rise from €82,400 (1996) to €384,247 (end-2006).

Interest rates have risen in tandem with the rest of the Eurozone, moving from 2.25% in December 2005, to 4.0% in June 2007.

Yields across Ireland have averaged 3.1%, according to the most recently bi-annual Daft Report (update expected February). These yields are comparatively speaking very low.

There has also been significant overbuilding. The numbers of dwellings completed has risen very sharply, more than doubling from 30,000 in 1995 to nearly 81,000 in 2005. A third of current housing stock has been built since 1992. During 2007, the stock of houses for sale rose 62%, and transaction volumes fell drastically, according to the most recent Daft report.

The developers have responded, and in 2007 the number of new homes started fell 47% compared with last year. For December, only 925 new homes were registered, down 60% on the same month a year earlier - the lowest monthly figure since records began in 1995.

Gross yields in Dublin are somewhat higher than elsewhere in Ireland, at around 4%. Is this a crisis level?

Readers will know that the Guide gets uncomfortable when yields drop below 5%, significantly uneasy at 4%, and really worried by yields dropping to 3%.

In much of Ireland, current yields levels are at levels which worry us.

True, Ireland is a stable developed country (historical yield figures are unavailable, so it is hard to see whether there has been significant yield compression), its growth and stability justifies somewhat low yields. Central Dublin’s per square meter prices of €3,750 to €5,000 are also high, but arguably not perilously so.

But such low yields make a market very exposed when interest rates rise, especially when the market is largely floating rate. And interest rates have risen – and the market has responded.

Most mortgage loans are variable interest rate (78%). Most fixed-interest mortgages are for periods less than three years (60% of the total). Such high proportions of variable and short-term fixed rates are inherently dangerous.

However, the Bank of England did not accept mortgage-backed debt as collateral in similar lending operations until after the run on Northern Rock.

However, the Bank of England did not accept mortgage-backed debt as collateral in similar lending operations until after the run on Northern Rock.

Jean-Claude Trichet, president of the ECB, last week insisted the central bank had not been bailing out banks in Spain, but said that there had been a marked increase use of securitised bonds as collateral by Spanish banks and others.

Bank of England lending to UK banks grew by about £6.2bn over the same period, but there is no data on the collateral used. In the US, the Federal Home Loan Bank has pumped $750bn into the system by extending longer-term funding direct to mortgage lenders, such as Countrywide.

The big difference is that European banks must re-raise this funding every week and the mortgage- backed bonds pledged at the ECB eventually will have to find their way to the capital markets, which many analysts believe could mean that markets such as Spain are potentially storing up problems for the future.

While markets for securitised debt remain closed, it is difficult to put a price on European mortgage-backed securities and banks in the region can be much slower to mark down the value of holdings of such bonds. By accepting them in exchange for cash, the ECB may be delaying the repricing of risk that analysts believe is necessary for the orderly resumption markets in such debt.

"The credit markets have been on heroine and while the US solution is put them through cold turkey, the Europeans want to put them on methadone," said one London-based economist.

> Toro has some more thoughts & data on spain

> Toro hat noch weitere Gedanken und Detail zum Thema Spanien

Handelsblatt FRANKFURT. Die angeschlagene Mittelstandsbank IKB braucht erneut eine milliardenschwere Kapitalspritze, um das Überleben der Bank zu sichern und die Kapitalbasis zu stärken. „Die Situation ist kritisch“, sagte ein Insider. Es gehe um ein drittes Rettungspaket in Höhe von bis zu 1,75 Mrd. Euro.

Noch gebe es aber keine Einigung der Beteiligten: "Alles ist im Fluss." Am Mittwoch tagt Finanzkreisen zufolge der 37-köpfige Verwaltungsrat der KfW, die mit rund 38 Prozent der größte Anteilseigner der IKB ist.

Das neue Rettungspaket ist Finanzkreisen zufolge aktuell Gegenstand von Verhandlungen zwischen KfW, der mit knapp zwölf Prozent beteiligten Stiftung Industrieforschung sowie den privaten Banken, die im Bundesverband deutscher Banken (BdB) organisiert sind. Unklar sei aber, ob nicht auch der Bund einspringen müsse. So spreche die KfW auch mit der Regierung über eine mögliche Unterstützung. Grundsätzlich reiche das Eigenkapital der KfW zwar aus, um entsprechend ihrem Anteil die IKB erneut zu retten, hieß es. Seit der letzten Unterstützungsaktion nähere sich der Kapitalbedarf aber der Grenze, ab der es nicht mehr hundertprozentig auszuschließen sei, dass die IKB -Krise den Eigenkapitalanteil, mit dem die ERP-Mittelstandsprogramme abgesichert sind, berühren könnte. Der Bund solle sicherstellen, dass dies nicht passieren könne.

Vorsitzender des Verwaltungsrats der KfW ist seit Jahresbeginn Bundeswirtschaftsminister Michael Glos (CSU). Das Wirtschaftsministerium wollte sich auf Anfrage nicht zur neuerlichen IKB -Krise äußern. Auch IKB, BdB und KfW lehnten eine Stellungnahme ab.

Die IKB war wegen milliardenschwerer Engagements im US-Subprime-Markt in die Krise geraten und konnte im Juli vergangenen Jahres nur durch das Eingreifen der deutschen Kreditwirtschaft vor dem Zusammenbruch gerettet werden. Seither wurden der Düsseldorfer Bank Garantien über sechs Mrd. Euro gewährt, rund fünf davon trägt die staatliche KfW. Der BdB kommt auf etwa eine halbe Mrd. Euro, auch Sparkassen und Genossenschaftsbanken sind beteiligt. Diese hatte aber bereits nach der letzten Rettungsaktion klar gemacht, für weitere Hilfen nicht zur Verfügung zu stehen. Als privates Institut wäre bei einem Zusammenbruch der BdB rein formal - neben den Eigentümern - ohnehin in der Hauptverantwortung.

Finanzkreisen zufloge wäre eine Pleite der IKB mittlerweile günstiger, als die langwierige und aufwändige Rettung des Institut. Aus politischen Gründen sei dies jedoch nicht akzeptabel. "Es wäre ein sehr schlechtes Zeichen für die Märkte, wenn eine deutsche Bank pleite geht", sagte ein Insider.

The owners of WestLB AG have reached an agreement to ring-fence substantial risks in the Bank´s structured portfolios. Securities with a nominal volume of roughly € 23 billion will be ring-fenced off the Bank´s balance sheet in a special purpose vehicle.

The financing of the special purpose vehicle will be secured by a guarantee from the owners of up to € 5 billion to cover any payment defaults. The owners will meet any possible losses from these securities portfolios in line with their shareholdings in WestLB up to an amount of € 2 billion, in compliance with their statement of January 20, 2008. Any further losses up to € 3 billion will be borne by the State of North Rhine-Westphalia

Die Eigentümer der WestLB AG haben beschlossen, die Bank von wesentlichen Risiken aus ihren strukturierten Portfolien zu befreien. Dazu werden die Papiere in einem Volumen von etwa nominal 23 Mrd. € in einer Zweckgesellschaft außerhalb der Bank gebündelt

Die Finanzierung der zu gründenden Zweckgesellschaft wird durch eine Garantie der Eigentümer für tatsächliche Zahlungsausfälle in Höhe von bis zu 5 Mrd. € bgesichert. Die Eigentümer tragen etwaige Verluste aus diesen Wertpapierportfolien entsprechend ihren Anteilen an der WestLB bis zur Höhe von 2 Mrd. € in Erfüllung ihrer Erklärung vom 20.1.2008. Darüber hinaus gehende Verluste von bis zu 3 Mrd. € werden vom Land NRW getragen

Quote December West LB related to the SIV / Zitat Dezember West LB

“We are also convinced that the assets that Kestrel and Harrier have could be more highly valued, but that the market is not ready for that.”

LOL!!!!

WestLB Owners Agree to Bailout as Bank Seeks a Merger Bloomberg

Steuerzahler muss für WestLB-Rettung bluten FT Deutschland

FT Alphaville Banks’ exposures through bond insurers, or monolines, is far from limited to mortgage-related MBS and muni bonds. There’s a third big exposure - to leveraged buyout loans - that banks will have to deal with if monolines hit the rocks.

FT Alphaville Banks’ exposures through bond insurers, or monolines, is far from limited to mortgage-related MBS and muni bonds. There’s a third big exposure - to leveraged buyout loans - that banks will have to deal with if monolines hit the rocks. Monolines, of course, are no longer in a position to be writing new contracts for banks to use as one half of their negative basis trades. The consequence of that has been that banks have stopped buying AAA tranches of CLOs. Unable to sell those, CLOs have faltered and banks in turn, have found themselves with lots of big buyout loans stuck on their books. No new financing is available for private equity deals.

Monolines, of course, are no longer in a position to be writing new contracts for banks to use as one half of their negative basis trades. The consequence of that has been that banks have stopped buying AAA tranches of CLOs. Unable to sell those, CLOs have faltered and banks in turn, have found themselves with lots of big buyout loans stuck on their books. No new financing is available for private equity deals. > Deutsche Bank was very optimistic in yesterdays call to unload all the € 21 bln loans with no losses. They argue that the quality of the loans is high and that it is and has always been the policy from Deusche to take 10 percent of the structured loans onto their books to signal that they have full confidence in their underwriting standarts. I think they are way too optimistic.....

> Deutsche Bank was very optimistic in yesterdays call to unload all the € 21 bln loans with no losses. They argue that the quality of the loans is high and that it is and has always been the policy from Deusche to take 10 percent of the structured loans onto their books to signal that they have full confidence in their underwriting standarts. I think they are way too optimistic..... > Die Deutsche Bank has sich gestern in der Analystenkonferenz extrem optimistisch gezeigt das sie die knapp 21 Mrd € an Unternehmenskrediten die sich in Folge des Private Equity Übernahmewahnsinns angehäuft haben ohne Verluste weiterreichen kann. Argumentiert wird das die Qualität hoch sei und das es seit jeher Politik der Deutcshen Bank ist jeweils 10 % der so strukturierten Verkäufe in die eigenen Bücher zu nehmen. Damit soll unterstrichen werden das man vollstest Vertrauen in die Kreditprüfung hat. Löblich...... Denke trotzdem das hier sicher noch einige gewaltige Abschreibungen kommen werden.

Even if monolines don’t crash and burn, banks will still have to make writedowns on these trades. As the value of the CDS written by the monoline decreases, so, too, will banks exposure to CLOs, and through them LBOs, have to increase. And higher exposures will also, of course, put pressure on capital.

And one final point: having set up one negative basis trade, it hasn’t been uncommon for banks to take out a CDS against the CDS counterparty in that trade. As Paul J Davies points out in today’s FT, through negative basis trades, banks’ monolines exposures have often been hedged with other monolines.

Update: The WSJ has an interesting number crunching piece on the state of the LBO industry - and the amounts banks are finding themselves stuck with.

Deutsche Bank reports net income of EUR 6.5 billion, up 7%, for the year 2007

Deutsche Bank reports net income of EUR 6.5 billion, up 7%, for the year 2007“In the fourth quarter, we again demonstrated the quality of our risk management. We had no net write-downs related to sub-prime, CDO or RMBS exposures. Those trading businesses in which we reported losses in the third quarter produced a positive result in the fourth quarter. In leveraged finance, where we had significant write-downs in the third quarter, net write-downs in the fourth quarter were less than EUR 50 million.”

{kind=link}